HELOCs have the benefit of being flexible and allowing you to make payments when needed. You can choose to make payments with a debit card, a check, cash from the bank, or an electronic transfer. Your payments are small during the draw period, and generally only include interest on the borrowed amount. HELOCs permit you to pay off the principal loan, but you will be charged fees if this happens.

Variations in interest rates are possible over time

HELOCs are a great way to access a line of credit with a low interest rate for an extended period of time. But, interest rates can change frequently so make sure you shop around to find the best interest rate for you. A slight change in interest rate can mean a significant difference in the total amount that you pay over the life of your loan.

HELOC interest rates can be variable. They are based on the prime rate and federal funds rate. The prime rate is generally three percentage point higher than the federal fund rate and lenders often base their HELOC interest rates on that.

A HELOC borrower can draw money from the line of credit for a period of 10 to 20 years. The borrower is allowed to make monthly payments until the loan is completely repaid.

Refinancing or closing an HELOC before the draw ends

If you use it correctly, a HELOC is a great financial tool. If you don't pay the loan off within the set time, it could become a trap. You can avoid this by reviewing the terms of the loan carefully. HELOCs can be variable-rate loans, meaning that the interest rate may change according to market conditions.

First, it's important to know the expiration date. HELOCs generally have a 20 Year draw period. The draw period is over and the repayment period begins. Many lenders allow you the option to make interest-only payment during the draw period. However, they may require that you make a minimum payment to include some principal.

Second, you need to know the terms of the loan prior to closing. Avoiding a prepayment penalty by refinancing or closing your HELOC before the draw ends is possible. A financial planner or lender can help you decide whether or not to shut down the account.

Tips for a successful time period of heloc drawing

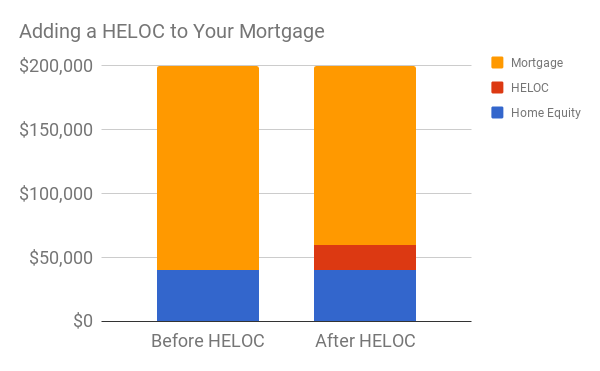

A HELOC, or Home Equity Loan, is an open line for credit that is based primarily on your home's equity. You can borrow as much as you like and have it paid off in as little as five to ten years. While you'll have to pay interest on the amount you borrow, the monthly payment can be lower than the amount you owe.

If you require a large sum of money to cover ongoing expenses, but aren't certain how much, you can apply for a HELOC multiple times. For instance, you might need lots of money to remodel your garage. This could include hiring contractors to redo the floors and purchasing cabinets. A painter may be needed to paint your garage. The HELOC lets you borrow the exact amount needed for your project.

FAQ

How do you calculate your interest rate?

Interest rates change daily based on market conditions. The average interest rates for the last week were 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

Do I require flood insurance?

Flood Insurance covers flood damage. Flood insurance helps protect your belongings and your mortgage payments. Learn more about flood coverage here.

What should I look for in a mortgage broker?

People who aren't eligible for traditional mortgages can be helped by a mortgage broker. They compare deals from different lenders in order to find the best deal for their clients. This service is offered by some brokers at a charge. Others offer no cost services.

Is it cheaper to rent than to buy?

Renting is generally less expensive than buying a home. However, you should understand that rent is more affordable than buying a house. A home purchase has many advantages. You will be able to have greater control over your life.

What is the cost of replacing windows?

The cost of replacing windows is between $1,500 and $3,000 per window. The cost to replace all your windows depends on their size, style and brand.

Do I need a mortgage broker?

A mortgage broker can help you find a rate that is competitive if it is important to you. Brokers are able to work with multiple lenders and help you negotiate the best rate. However, some brokers take a commission from the lenders. You should check out all the fees associated with a particular broker before signing up.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to Find Real Estate Agents

The real estate agent plays a crucial role in the market. They offer advice and help with legal matters, as well selling and managing properties. You will find the best real estate agents with experience, knowledge and communication skills. Look online reviews to find qualified professionals and ask family members for recommendations. A local realtor may be able to help you with your needs.

Realtors work with both buyers and sellers of residential real estate. It is the job of a realtor to help clients sell or buy their home. In addition to helping clients find the perfect house, realtors also assist with negotiating contracts, managing inspections, and coordinating closing costs. Most realtors charge a commission fee based on the sale price of the property. Unless the transaction is completed, however some realtors may not charge any fees.

There are many types of realtors offered by the National Association of REALTORS (r) (NAR). NAR members must pass a licensing exam and pay fees. Certified realtors are required to complete a course and pass an exam. NAR has established standards for accredited realtors.