A home equity line is similar to a primary mortgage. Lenders will ask about your equity in your home, the value of your home and your income before they approve your loan application. Lenders must verify that borrowers aren't credit risk before they approve loans. They also want to know the value of the collateral, which is your home.

Getting a home equity line of credit

A home equity line credit is a good option to finance major expenditures such as home improvement or tuition. Its prime rate is set by the Federal Reserve. The Federal Funds Interest Rate is generally 3% above the prime rate. The interest rate on home equity lines of credit may also be tax deductible.

A home equity loan allows borrowers to borrow cash based upon the home's worth, which is usually $50,000. This is similar to a credit line, except that you only pay interest for the amount you use. You may also get discounts depending on how much you use your home equity line credit.

Good credit is required to be approved for a home equity line credit. While most lenders accept credit scores above 700, some will consider borrowers who have less credit. To get the best interest rates, it's important that your credit score is as high as you can. Additionally, a home equity loan of credit allows you to access larger funds than personal loans or credit cards.

Repayment period

You should take into account a variety of factors when determining the repayment terms for a home equity loan. First, make sure that you have enough equity in your home to qualify for the loan. It is also important to ensure you can afford the increased monthly payment. Also, keep in mind your debt to income ratio and credit score when making this decision.

The repayment period for a home equity credit line is typically 5 to 10 year. During this time, you will make monthly payments that include principal and interest. This will enable you to pay off your debt quicker and lower the monthly payment. Depending on your personal situation, you might also consider a payment program to lower your monthly payments.

HELOCs allow you to borrow money up to a maximum of $2,500 depending on the amount of your home and your mortgage balance. Your financial adviser should be consulted to confirm that you can afford the loan. Also, keep in mind that a HELOC may be unsuitable if you plan to sell the house.

Interest rate

A home equity loan is a type if credit secured by the homeowner's home. Variable interest rates depend on many factors like creditworthiness, loan value ratio and loan amount. There are a few things that you can do to ensure the best rate.

First, it is important to understand how the loan works. A home equity line of credit typically has two phases: a draw period and a repayment period. The draw period is usually for around 10 years. You will typically make smaller interest-only payments during this period, with any additional payments going towards the principal.

The home equity line-of credit (HELOC), is similar to a creditcard, but you pay interest only on the amount that you spend and not the entire loan amount. The interest rate for a HELOC is usually lower that a traditional mortgage or other types. HELOCs also have the advantage of not having to repay the whole amount immediately.

FAQ

What is the maximum number of times I can refinance my mortgage?

It all depends on whether your mortgage broker or another lender is involved in the refinance. You can typically refinance once every five year in either case.

Can I get a second loan?

Yes. But it's wise to talk to a professional before making a decision about whether or not you want one. A second mortgage can be used to consolidate debts or for home improvements.

Can I buy a house without having a down payment?

Yes! Yes! There are many programs that make it possible for people with low incomes to buy a house. These programs include FHA, VA loans or USDA loans as well conventional mortgages. Check out our website for additional information.

Statistics

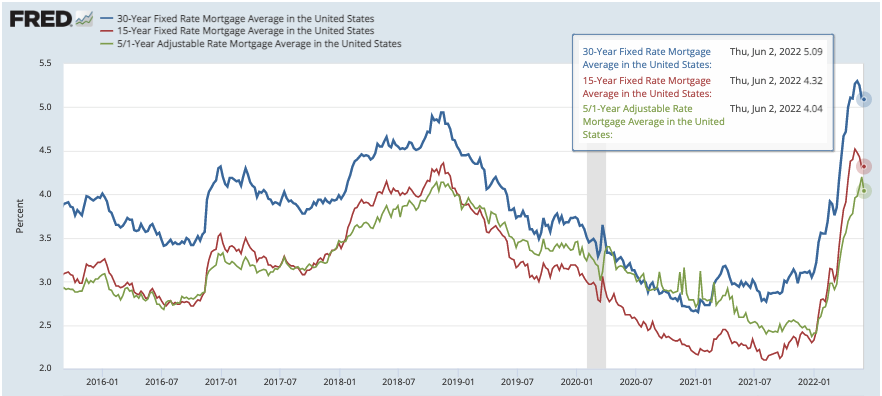

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to find real estate agents

Real estate agents play a vital role in the real estate market. They offer advice and help with legal matters, as well selling and managing properties. You will find the best real estate agents with experience, knowledge and communication skills. Online reviews are a great way to find qualified professionals. You can also ask family and friends for recommendations. Consider hiring a local agent who is experienced in your area.

Realtors work with buyers and sellers of residential properties. The job of a realtor is to assist clients in buying or selling their homes. A realtor helps clients find the right house. They also help with negotiations, inspections, and coordination of closing costs. Most realtors charge a commission fee based on the sale price of the property. Unless the transaction is completed, however some realtors may not charge any fees.

The National Association of REALTORS(r) (NAR) offers several different types of realtors. NAR requires licensed realtors to pass a test. Certification is a requirement for all realtors. They must take a course, pass an exam and complete the required paperwork. NAR recognizes professionals as accredited realtors who have met certain standards.