A down payment calculator is a tool that helps buyers calculate the amount they need to pay for their down payment. This calculator lets you input the price of the house, the downpayment percentage, and the monthly rent payment to calculate the downpayment percentage. Once buyers have an idea of the amount they will need to buy a home, they can use the down payment calculator for a budget.

Renter budget equivalent calculator

To determine your mortgage affordability, you will need to first calculate whether you can afford to rent and then buy a home. To determine if you are able to afford a mortgage, use a renter budget equivalent downpayment calculator. This calculates your rent payments. You can enter your current rent payment as well as future mortgage payments. You can also input property taxes and annual insurance costs.

Rent can be paid up to 40% of your average income if your income exceeds the median. Renting will give you more space and better locations. You will need to carefully monitor your spending and decide if you can afford to pay more. You should also carefully assess your financial situation before you sign a lease.

Cost of mortgage insurance

The best way to calculate the cost for mortgage insurance is to use a down payment calculator. This insurance is typically paid by the borrower and is based on their FICO credit score. Before deciding how much mortgage insurance a borrower should have, mortgage lenders will consider several factors. A borrower with a small downpayment may not need mortgage insurance.

Different insurance companies have different rates for PMI. A borrower can find a lower or greater rate by shopping around. The cost of a loan will also be affected by the lender's discretion and the amount. Before choosing a PMI program, it is best that you speak to an experienced loan officer.

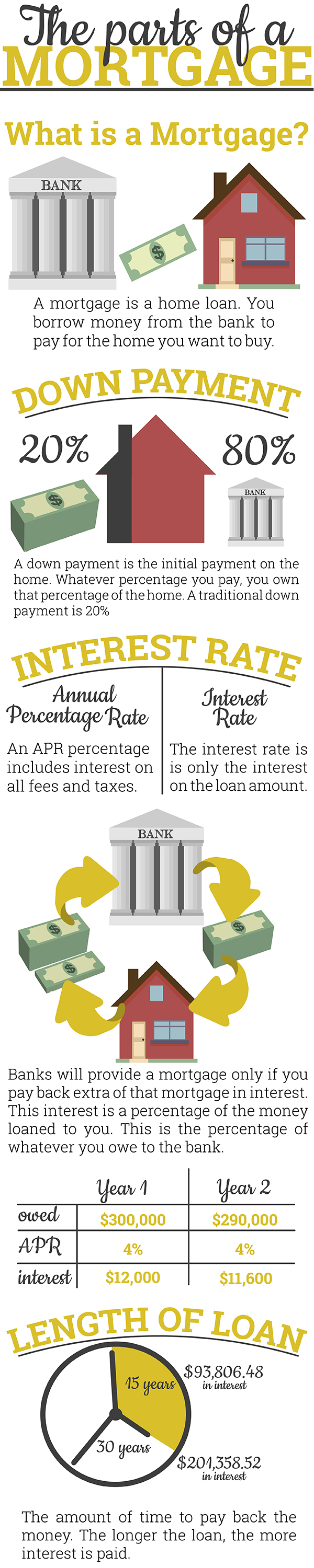

Deposit amount

A downpayment calculator is a valuable tool that can help you figure out how much you should put down on a house. Because borrowers with longer repayment terms are likely to pay less interest, larger down payments can be more beneficial. A large down payment may not be a good idea when you need to sell the house or refinance it.

The calculator allows you input the price of the house you are interested in buying and will then show you how much you can save. You can enter a percentage of the purchase price, or a specific amount.

Taxes

When calculating the cost to purchase a home, it is important to use a down payment calculator. Unlike a credit card, a down payment is the only payment you'll make upfront during the home purchase process. There are additional costs, including points of your loan and insurance. Lender's title insurance and appraisal fees. These costs could add up to three percent to the purchase price.

PMI

Many homebuyers have difficulty saving for 20% down payments. PMI loans let them buy a home with a lower downpayment, and they can then cancel the loan once their 20% equity has been built up. The PMI fee is a percentage of the loan amount. It can vary from 0.3% up to 1.5% depending on your credit rating and down payment amount. If you have more equity than 20%, your lender may cancel PMI.

PMI is usually paid as a monthly premium, or at closing. You may also opt to pay it in advance. If you're considering paying the PMI upfront, a PMI and down payment calculator can help you determine the amount you'll need to put down as well as an amortization schedule. A mortgage insurance calculator does not replace professional advice. For more information or advice, consult a loan officer.

FAQ

What should you consider when investing in real estate?

First, ensure that you have enough cash to invest in real property. If you don’t have the money to invest in real estate, you can borrow money from a bank. You also need to ensure you are not going into debt because you cannot afford to pay back what you owe if you default on the loan.

You must also be clear about how much you have to spend on your investment property each monthly. This amount should include mortgage payments, taxes, insurance and maintenance costs.

Also, make sure that you have a safe area to invest in property. It is best to live elsewhere while you look at properties.

What are the three most important factors when buying a house?

The three most important things when buying any kind of home are size, price, or location. Location refers the area you desire to live. Price refers how much you're willing or able to pay to purchase the property. Size refers to how much space you need.

Can I get another mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

What is a reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. It allows you to borrow money from your home while still living in it. There are two types to choose from: government-insured or conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. FHA insurance will cover the repayment.

What is the average time it takes to sell my house?

It depends on many factors including the condition and number of homes similar to yours that are currently for sale, the overall demand in your local area for homes, the housing market conditions, the local housing market, and others. It can take anywhere from 7 to 90 days, depending on the factors.

How much will it cost to replace windows

Replacement windows can cost anywhere from $1,500 to $3,000. The cost to replace all your windows depends on their size, style and brand.

What are the advantages of a fixed rate mortgage?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This guarantees that your interest rate will not rise. Fixed-rate loans come with lower payments as they are locked in for a specified term.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to become an agent in real estate

You must first take an introductory course to become a licensed real estate agent.

Next, you will need to pass a qualifying exam which tests your knowledge about the subject. This requires that you study for at most 2 hours per days over 3 months.

You are now ready to take your final exam. You must score at least 80% in order to qualify as a real estate agent.

You are now eligible to work as a real-estate agent if you have passed all of these exams!