You might be curious about the benefits of VA home loans. This type of loan is guaranteed by the government and can be approved quickly. Borrowers benefit from this guarantee because it makes it easy to obtain a loan. But even though the government guarantees the loan, it doesn't protect borrowers from default. You can lose your home to foreclosure if you default on the loan. There is good news: The VA has dedicated staff to assist you in times of need.

No down payment

VA loans are a great option because there is no downpayment. However, some restrictions apply. You must be a current or former member of the armed forces. If you are first-time homebuyer or borrow more money than the conforming loan limits, you might need to pay a down payment.

You are at risk of losing your emergency savings in the event you lose your job or have to take out a downpayment. Make sure you consider your budget and long term financial goals before you make a decision on whether to make a payment for your VA Loan loan.

No mortgage insurance

The best thing about a VA loan is the fact that you don’t need to pay mortgage insurance. As long as your requirements are met, you will be able purchase upto $ without any downpayment and without a mortgage policy. This is especially important for first-time buyers.

VA loans could save you thousands of bucks over the life-of the loan. While you must still pay a small VA funding fee (a percentage of the loan amount) at the time of closing, the money is rolled into the loan balance, so you won't have to worry about it right away.

Low interest rate

Veterans may be eligible to receive a VA loan at a reduced interest rate. The Veterans Administration guarantees these loans. They offer low rates and can make purchasing a home affordable. Your credit score, credit history, financial situation, and other factors will affect the VA's loan rates. To reduce your interest rate you can also make a downpayment.

You can find the best interest rate for your VA loan by shopping around. It is important to have a good credit score, as this will improve your chances of qualifying for a low interest rate on a VA mortgage. It is also important to shop around and compare mortgage offers from different lenders.

Requirements for down payments

If you're a veteran or have a surviving spouse, you may want to consider a down payment when applying for a VA loan. Making a down payment can increase your chances of qualifying for the loan. Lenders tend to view borrowers with down payments as less likely to default on the mortgage. Down payments aren't required for all VA loans, but they can improve your chances of getting approved for the loan.

A down payment can be a good indicator of the borrower's willingness to pay for the loan. A small downpayment can make a difference if the buyer has poor credit, past credit problems, or a credit history that isn't perfect. VA mortgages don't require private mortgage coverage, which can add up to hundreds of dollars per year for FHA and conventional loans.

FAQ

How do you calculate your interest rate?

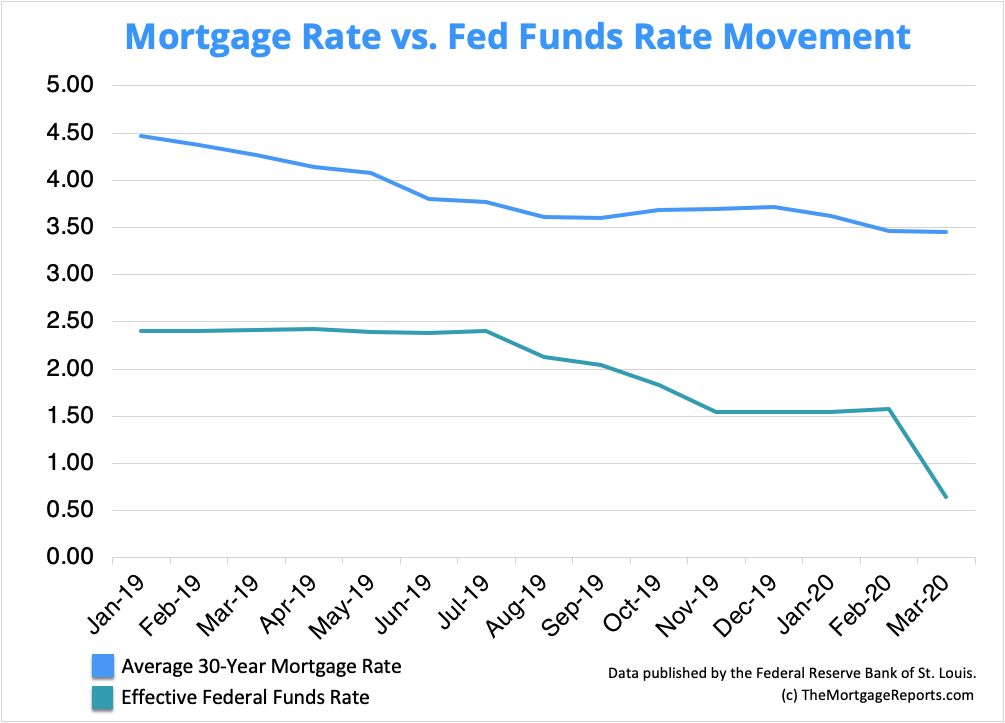

Market conditions affect the rate of interest. The average interest rate over the past week was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. For example, if $200,000 is borrowed over 20 years at 5%/year, the interest rate will be 0.05x20 1%. That's ten basis points.

How much money will I get for my home?

The number of days your home has been on market and its condition can have an impact on how much it sells. Zillow.com says that the average selling cost for a US house is $203,000 This

How do I eliminate termites and other pests?

Over time, termites and other pests can take over your home. They can cause damage to wooden structures such as furniture and decks. This can be prevented by having a professional pest controller inspect your home.

What should I be looking for in a mortgage agent?

A mortgage broker helps people who don't qualify for traditional mortgages. They compare deals from different lenders in order to find the best deal for their clients. Some brokers charge fees for this service. Others provide free services.

Is it possible to get a second mortgage?

Yes, but it's advisable to consult a professional when deciding whether or not to obtain one. A second mortgage is often used to consolidate existing loans or to finance home improvement projects.

Is it cheaper to rent than to buy?

Renting is typically cheaper than buying your home. However, you should understand that rent is more affordable than buying a house. The benefits of buying a house are not only obvious but also numerous. You will have greater control of your living arrangements.

What is a Reverse Mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It allows you access to your home equity and allow you to live there while drawing down money. There are two types of reverse mortgages: the government-insured FHA and the conventional. You must repay the amount borrowed and pay an origination fee for a conventional reverse loan. FHA insurance covers repayments.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to locate an apartment

Finding an apartment is the first step when moving into a new city. This involves planning and research. This includes researching the neighborhood, reviewing reviews, and making phone call. Although there are many ways to do it, some are easier than others. The following steps should be considered before renting an apartment.

-

You can gather data offline as well as online to research your neighborhood. Online resources include Yelp. Zillow. Trulia. Realtor.com. Online sources include local newspapers and real estate agents as well as landlords and friends.

-

Read reviews of the area you want to live in. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. You may also read local newspaper articles and check out your local library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what the best and worst things about the area. Ask for their recommendations for places to live.

-

Take into account the rent prices in areas you are interested in. Consider renting somewhere that is less expensive if food is your main concern. On the other hand, if you plan on spending a lot of money on entertainment, consider living in a more expensive location.

-

Find out about the apartment complex you'd like to move in. It's size, for example. How much is it worth? Is it pet friendly What amenities does it offer? Can you park near it or do you need to have parking? Do you have any special rules applicable to tenants?