Home equity loans are secured installment loans you can take out against the home's value. These loans have a fixed rate of interest, fees, and are less flexible that home equity lines. There are some important steps to follow if you want to apply for a home equity mortgage.

Fixed-rate, fixed-rate installment loans secured with your home's equity are called home equity loans.

A home equity loans is a loan that's secured by your home. These loans have fixed interest rates and long loan terms, making payments predictable. These loans can be a great option for those who need to consolidate debt and are facing large monthly expenses. You may also be able to deduct your taxes from home equity loans.

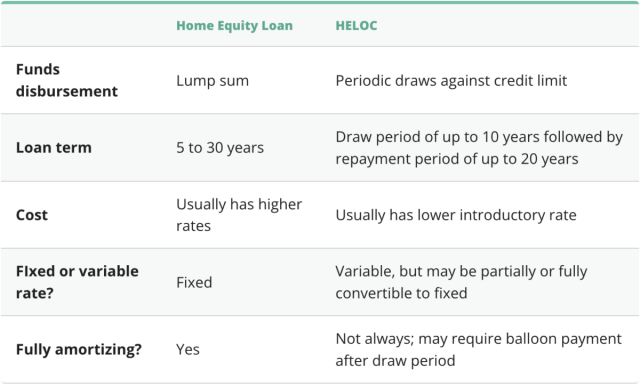

A home equity loan can often be more affordable than a HELOC. The interest rate is set, unlike an HELOC whose rates can vary depending on national benchmarks. These loans are ideal for small loans, but not for large purchases. Home equity loans have fixed interest rates, which can help you better manage finances.

They are subject to a variable interest rate

Variable interest rates should be considered when applying for a home equity mortgage. A loan can be approved even if you have a low credit score. However, these loans will come with higher fees and interest rates. A low credit score could also indicate that you are unable to repay the loan. This has resulted in stricter lending policies and increased restrictions for this type of loan.

Variable rate home equity loans come in many forms including HELOCs which function like a credit card. HELOCs' interest rates fluctuate with the prime interest. Your payments will depend upon the interest rates, the length of the loan repayment, and the amount that you borrow. HELOCs can have a draw term of up to 10 year. HELOCs sometimes offer a low initial interest rate.

They charge more

In many ways, home equity loans differ from personal loans. First, they're easier to get than personal mortgages and second, they're less risky. A home equity loan is secured by the homeowner, giving the lender greater protection if the borrower defaults. Home equity loans often have lower interest rates.

The fees associated with home equity loans also vary from lender to lender. Some lenders charge an origination fee to apply for a loan. Others add it to the total loan cost. These fees may range in price from $0 to $225. In addition, some lenders charge an application fee to complete the loan application. Credit report fees are another cost associated with home equity loans. They usually amount to about $25.

They are less flexible then a home equity line credit.

A home equity line is similar to a credit card. You can access the money as you need it while it's available. You can draw on the money at any time during the draw. Some lenders will even allow interest-only payments. While it may increase your monthly payment, it can help you repay the credit.

A home equity loan can also have a negative effect on your credit score. A home equity loan will have a greater impact than a line of credit, but it all depends on how much your home owes and the interest rate. A minimum credit score of 620 is required by lenders, but some lenders will accept borrowers with lower credit scores. Your credit score will determine the loan terms and interest rates.

They can help you consolidate debt

If you're looking to consolidate debt, a home equity loan may be a great option for you. Debt consolidation is a great way to reduce your payments and lower your interest rates. This type of loan is typically lower than other types of loans, and the interest you pay may even be tax-deductible. It is an excellent option for high interest credit card balances and people looking to reduce their expenses. But, this type of loan has its risks. This loan could not be paid off and you could lose the home you have saved.

A debt consolidation loan allows you to combine multiple debts into one loan, with one interest rate. Also, one monthly payment. This loan is available from a variety of lenders, including credit unions and banks. Online applications are also available from some lenders for consolidation loans. Some of these sites offer same-day approval, making the process even faster.

FAQ

Are flood insurance necessary?

Flood Insurance protects against damage caused by flooding. Flood insurance can protect your belongings as well as your mortgage payments. Learn more about flood insurance here.

Is it better buy or rent?

Renting is generally cheaper than buying a home. However, you should understand that rent is more affordable than buying a house. Buying a home has its advantages too. For instance, you will have more control over your living situation.

How long does it take for my house to be sold?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It may take up to 7 days, 90 days or more depending upon these factors.

What is the maximum number of times I can refinance my mortgage?

It depends on whether you're refinancing with another lender, or using a broker to help you find a mortgage. Refinances are usually allowed once every five years in both cases.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

External Links

How To

How to be a real-estate broker

The first step in becoming a real estate agent is to attend an introductory course where you learn everything there is to know about the industry.

Next, pass a qualifying test that will assess your knowledge of the subject. This means that you will need to study at least 2 hours per week for 3 months.

Once you have passed the initial exam, you will be ready for the final. To become a realty agent, you must score at minimum 80%.

These exams are passed and you can now work as an agent in real estate.