A mortgage calculator can help you compare various mortgages. It allows you to compare interest rate, closing costs, as well loan terms. You can also select the loan with the lowest cost and the longest term. There are many mortgage calculators, and many lenders offer different terms. To get the best deal, it is crucial to choose the right mortgage calculator.

Comparing interest rates

The mortgage comparison calculator can prove to be very useful when shopping for a loan. These calculators will give you an idea of the total cost of a loan and the interest rate. It is important you take into account the total loan cost, including any fees or taxes. They also calculate the annual percentage rate, or APR, for each mortgage. A mortgage comparison calculator will help you decide which mortgage is best for you.

A mortgage comparison calculator is a great tool to help you compare different mortgage rates, loan terms, or monthly payments. By entering your current loan amount, interest rate, and loan term, you can then compare the interest rates of various lenders and decide which one is the best for your situation. You can use the same mortgage comparison calculator to compare two loans at once, or compare two or more loans with different terms.

Comparing closing prices

A mortgage calculator is a great tool to determine the best mortgage rate and closing cost. Closer costs are fees that you must pay to the lender. Mortgage rates are the interest you pay each month to your lender. Many times, you can negotiate lower rates in exchange for lower closing fees.

You can input multiple loan terms into the mortgage calculator to quickly compare the monthly payment. It will also give you an estimate of how much interest you will pay over the term of the loan. This information will help you choose the right mortgage.

Selecting the lowest-cost loans

Homebuyers should choose the lowest-cost mortgage. This is because the interest rate has a huge impact on how much each month you will pay. A mere 0.25% increase in interest rates can result in a loan amount that is $14,000 more over the course of the loan's life.

FAQ

Is it possible to sell a house fast?

If you have plans to move quickly, it might be possible for your house to be sold quickly. However, there are some things you need to keep in mind before doing so. You must first find a buyer to negotiate a contract. You must prepare your home for sale. Third, your property must be advertised. Lastly, you must accept any offers you receive.

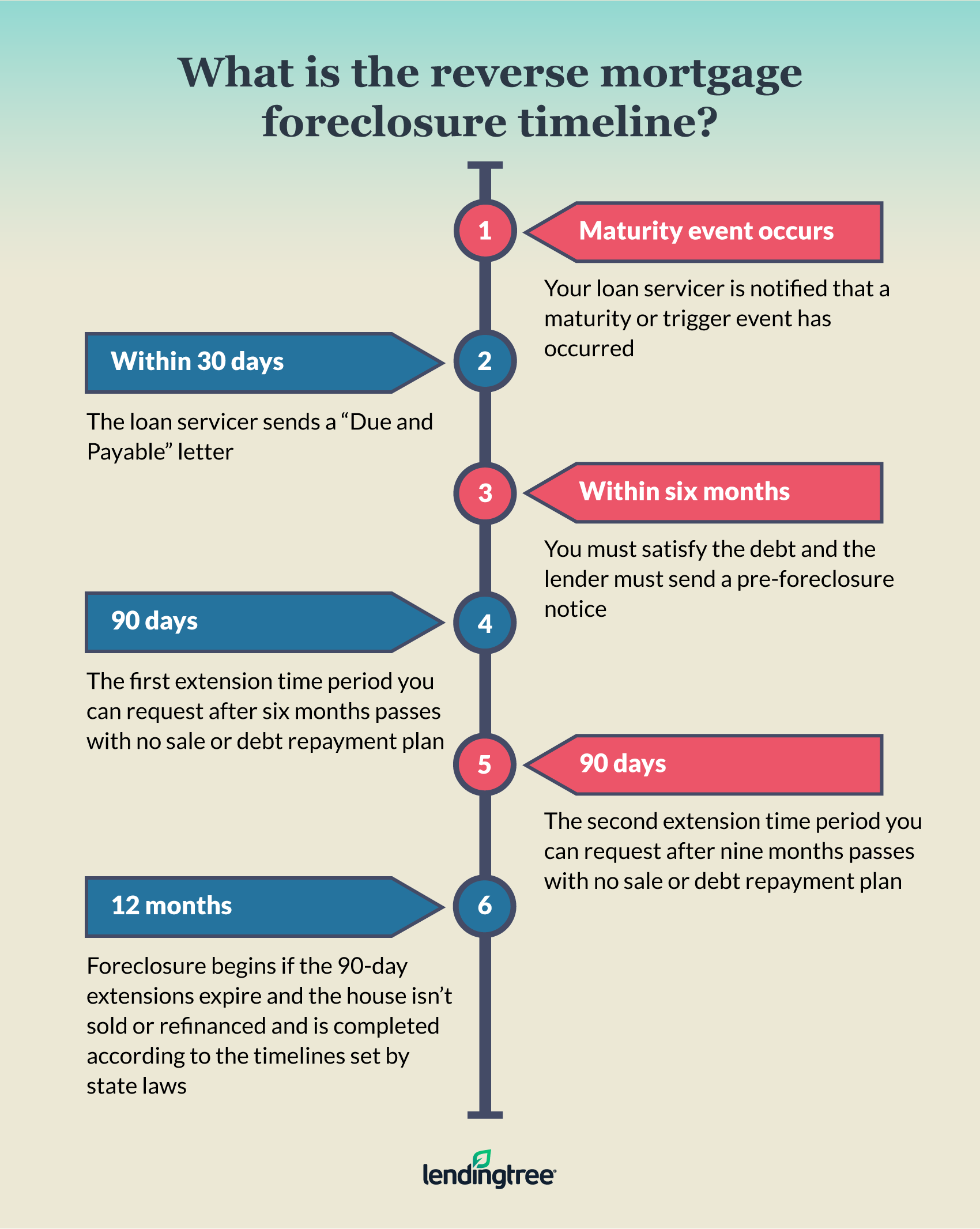

What is a Reverse Mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. If you choose FHA insurance, the repayment is covered by the federal government.

What are the top three factors in buying a home?

When buying any type or home, the three most important factors are price, location, and size. Location refers to where you want to live. Price is the price you're willing pay for the property. Size is the amount of space you require.

What are the key factors to consider when you invest in real estate?

The first thing to do is ensure you have enough money to invest in real estate. If you don’t have the money to invest in real estate, you can borrow money from a bank. Also, you need to make sure you don't get into debt. If you default on the loan, you won't be able to repay it.

You also need to make sure that you know how much you can spend on an investment property each month. This amount must be sufficient to cover all expenses, including mortgage payments and insurance.

Also, make sure that you have a safe area to invest in property. It would be a good idea to live somewhere else while looking for properties.

What is the maximum number of times I can refinance my mortgage?

This depends on whether you are refinancing with another lender or using a mortgage broker. You can refinance in either of these cases once every five-year.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to become real estate broker

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

Next, pass a qualifying test that will assess your knowledge of the subject. This requires studying for at minimum 2 hours per night over a 3 month period.

After passing the exam, you can take the final one. You must score at least 80% in order to qualify as a real estate agent.

Once you have passed these tests, you are qualified to become a real estate agent.