Home equity financing lets you use your equity for many purposes. These options can help increase your earning capacity and save you money on interest, payments, and other types debt. These loans allow you to make significant home improvements and add worth to your property.

Refinance via cash-out is a "primary" mortgage

A cash-out mortgage is one that gives additional cash upon closing. A cash-out refinance can be beneficial in many ways. One advantage is that it lowers your interest rate. Another advantage is that it lets you make changes to your loan terms and rates. To cut interest costs, you could change the length or term of your loan. A cash-out refinance also provides you with more money than you initially borrowed, which can be used for home improvements.

Cash-out refinances require that you have significant equity in your house. The lender will use your loan/to-value ratio to calculate this. You will also need to meet the lender's credit-score requirements. A new application will be required and all financial documents must be submitted.

A "second mortgage" can be obtained through a home equity loan.

A home equity loans is a loan that's secured by your home's equity. These loans are separate and can only be used if you have a first mortgage. Because these loans create an additional payment on top your existing loan, they can also be known as a “second mortgage”. The amount of the loan will depend on your current home value and your existing mortgage.

The best way to finance large amounts of money is with home equity loans. Before applying for one, it is crucial to fully understand the differences between each. This article will discuss the differences between second mortgages and home equity lines of credit.

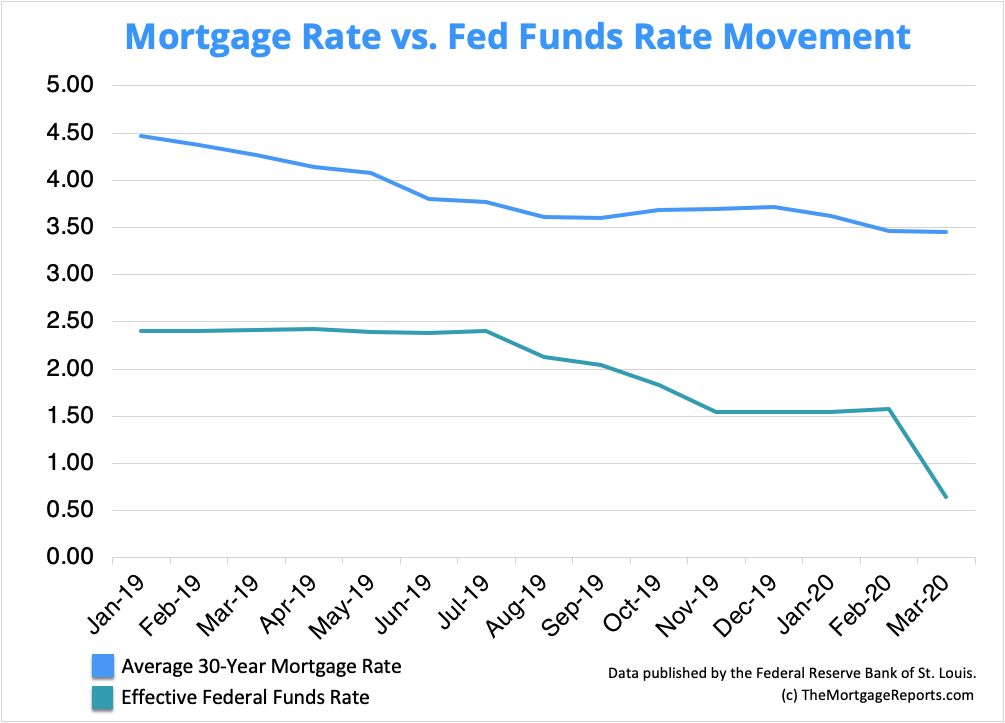

Interest rate

The interest rate of a home equity loan varies depending on several factors, including the current market interest rate, lender standards, and your personal finances. The interest rate you will pay is typically expressed as an annual percent rate (APR), which also includes closing costs and fees. In general, longer-term loans have higher interest rates that those of shorter duration.

For many borrowers, a home equity loan is a viable option. These loans can offer a fixed interest rate that you won't change, which can be helpful if you need a large lump sum of money quickly. You can budget for your payments and have lower interest rates with home equity loans than credit cards. You may want to consider a home equity loan for specific expenses, such as a major purchase or renovation.

You can avoid mortgage insurance

You can avoid mortgage insurance by taking out a home equity loans. First, don’t borrow more 80 percent of what your home is worth. Mortgage insurance is required if you borrow more than that. The good news about mortgage insurance is that rates have fallen in recent decades, which makes it easier for you to avoid this fee.

If you make a down payment of at least 20% on your home, you can also avoid paying mortgage insurance. This is the most common method, but you can also avoid mortgage insurance by making a minimum 20% down payment on your home. For instance, you can refinance your loan and use the equity in your home to avoid paying PMI. Prepay your mortgage.

FAQ

Is it possible to get a second mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is typically used to consolidate existing debts or to fund home improvements.

How can I calculate my interest rate

Market conditions influence the market and interest rates can change daily. The average interest rate for the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

Should I use an mortgage broker?

If you are looking for a competitive rate, consider using a mortgage broker. Brokers are able to work with multiple lenders and help you negotiate the best rate. Some brokers do take a commission from lenders. You should check out all the fees associated with a particular broker before signing up.

Statistics

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

For people looking to move, finding houses to rent is a common task. Finding the perfect house can take time. When you are looking for a home, many factors will affect your decision-making process. These factors include price, location, size, number, amenities, and so forth.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. For recommendations, you can also ask family members, landlords and real estate agents as well as property managers. You'll be able to select from many options.